Macroeconomic Risks in Equity Factor Investing

- Noël Amenc, Mikheil Esakia, Felix Goltz, And Ben Luyten

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Although not a new topic, the first half of the article explored and documented the dependent relationship between factor returns and time-varying macroeconomic environments.

In the second half of this paper, the authors provide insightful commentary and a renewed perspective on the potential for diversification across factors through the lens of assessing macroeconomic exposures. It is well known that factor returns are cyclical and can be negative for long periods. Because of this, it is common practice to combine factors that are not perfectly correlated in a simple model, such as Value and Momentum, into a multifactor strategy in order to reduce risk and smooth returns. This is all well and good unless those uncorrelated factors are in reality, regime dependent. In other words, what if the factors that appear uncorrelated on a simple basis become correlated right when you are counting on the diversification benefits 1. The authors find a number of unexpected patterns of exposures to macro regimes that should give pause to practitioners that rely on the use of conventional correlations across factor returns to determine potential diversifiers. The unconditional correlation may be a poor estimate of how any pair of factors will actually behave under specific macroeconomic conditions.

Seven economic state variables (the short rate, the term spread, the default spread, dividend yield, effective spread, price impact, and systematic volatility) are combined using a variety of regime classification methods to produce composite indicators of “good” and “bad” regimes. The purpose of using a number of classification methods is to reduce model risk (data mining) and to increase statistical rigor. Sensitivities to the resulting four regimes estimated where indicators of good/bad times were defined as follows:

- Risk Tolerance—if “good”, then the regime indicated is for an increase in risk tolerance and all 7 variables are used to classify;

- Macro Outlook—if “good”, then the regime indicated is for an improvement in the economic outlook and all 7 state variables are used;

- Macro Stability—if “good”, then the regime indicated is for a decrease in economic uncertainty and all variables except systematic volatility and dividend yield are used;

- Risk-on Conditions—if “good”, then the regime indicated is for a decrease in systematic volatility and a decrease in dividend yield; only systematic volatility and dividend yield are used.

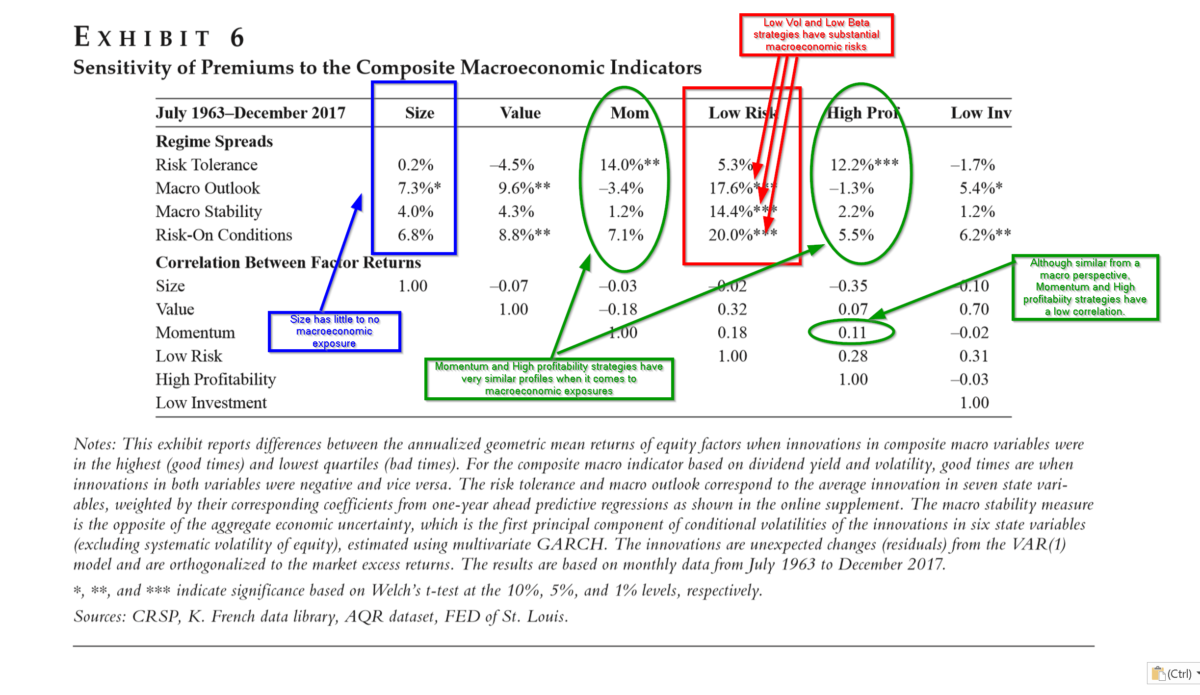

Five major insights with regard to the diversification potential across factors in the context of the four macroeconomic regimes emerged that are of interest to the practitioner and investor. Please refer to Exhibit 6 below.

What are the Academic Insights?

- Although low volatility and low beta strategies have been marketed as alpha-generating factors that are likely to produce “anomalous” return performance, they are likely to exhibit substantial positive sensitivity to 3 of the 4 regimes: macro outlook, macro stability, and risk-on conditions. Investors are unlikely to be aware of the significance of these risk exposures.

- The size factor, however, appears to have little to no sensitivity to any of the 4 macroeconomic regimes, making a size-based strategy an obvious candidate for inclusion in multiple factor portfolios for risk reduction purposes.

- Momentum and high profitability have very similar sensitivities to the 4 regimes in terms of size and sign. They also exhibit an especially strong sensitivity to the risk tolerance regime. The pairing of a momentum strategy with a high profitability strategy would likely offer little to no diversification potential in multiple factor portfolios.

- However, a pairing of either momentum or high profitability with factors that have little to no exposure to the risk tolerance regime suggests a different outcome. Four factors including value, low investment, and low vol/beta have very small and nonsignificant exposures to risk tolerance and likely would contribute to risk reduction when added to either a momentum strategy or to a high profitability strategy. For example, the authors report that combining high profitability with momentum would reduce risk by 23%; and combining high profitability with value would reduce risk by 27%; on average across factors.

- Factors with similarities in sensitivities to macro regimes may not always compare in a consistent manner to the unconditional correlation of pairs of factor returns. That is, factors with high correlations may not exhibit similar macro profiles when compared one to one. On the other hand, factors with low correlations may contemporaneously exhibit very similar macro sensitivities. It is then possible that a pair of factors may exhibit negative return performance during “bad” times even if they have a low unconditional correlation. Again, referring to the high profitability factor and the momentum factor, the return series between the two exhibits a low unconditional correlation of .11. They appear to be good diversifiers, however they each exhibit a strong sensitivity to risk tolerance regimes and almost no sensitivity to any of the other regimes. Obviously not the desired outcome if risk reduction is the objective. In contrast, high profitability also has a low unconditional correlation with value, .07, but exhibits opposite sensitivities in terms of the magnitude of the exposure and the sign of the exposure to macro regimes. Indeed, value has a significant and positive exposure to macro outlook (9.6%) and high profitability has a negative, although nonsignificant exposure to the same macro regime (-1.3%).

Why does it matter?

“Assessing regime dependency thus provides a fresh perspective on the diversification potential across factors.”

The fresh perspective from this paper goes a long way towards explaining why we need to better understand potential embedded macro risks in factor strategies. The sensitivities documented are substantial and therefore important for investors to recognize. The same exposures may exist in other strategies or in other asset classes unknown to investors but included in their portfolios all the same. The good news is that the sensitivities documented in this article differ in magnitude and sign across factors, thus providing a mechanism for identifying diversification potential across factors and for building portfolios with varying levels of exposure to specific regimes.

The most important chart from the paper

Abstract

There is a consensus that equity factors are cyclical and depend on macroeconomic conditions. To build well-diversified portfolios of factors, one needs to account for the fact that different factors may have similar dependencies on macroeconomic conditions. The authors provide a protocol for selecting relevant macroeconomic state variables that reflect changes in expectations about the aggregate economy. They show that returns of standard equity factors depend significantly on such state variables. Factor returns also depend on aggregate macroeconomic regimes reflecting good and bad times. These macroeconomic risks have strong portfolio implications. For example, some equity factors depend on interest rate risk. Investors who already have exposure to this risk through bond investments may increase loss risk when tilting to the wrong equity factors. The authors also show that standard multifactor allocations do not sufficiently address macroeconomic conditionality. Combining factors may not reduce macroeconomic risks even for factors with low correlation. Understanding macroeconomic risks is a prerequisite both for risk transparency and for improving diversification of equity factor investments.

Notes:

- The old: everything gets correlated in a bad market ↩