Factor Investing in Sovereign Bond Markets: Deep Sample Evidence

- Baltussen, Martens and Penninga

- working paper, 2021

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Despite government bonds being one of the major asset classes invested in global portfolios, 30% of overall market capitalization according to Doeswijk, et al. (2020), little work has been done to investigate whether factors are present in the sovereign bond market. (Here is a deep dive into fixed income factors by Ward). If factors are indeed present in the sovereign bond market do they add value and are they are persistent? This paper attempts at answering these research questions.

What are the Academic Insights?

One of the key features of this study is the extensive length of the sample: from January 1800 to December 2020: 221 years, a time frame with yields rising (wait, they can do that?) and falling cycles (different from other studies which covered a time frame dominated by falling yields). The research covers 16 developed government bond markets.

Several of the key results of the paper are as follows:

- Value and Momentum across bond markets ( country allocations), and Low-Risk on the bond curve ( maturity selection) offer attractive factor premiums, with Sharpe ratios of 0.51, 0.24, and 0.40 over the full sample.

- These factor premiums are consistent over time, being positive in 72% (Momentum) to 92% (Value) of 10-year rolling periods.

- Combining the factors into a simple multi-factor portfolio gives a highly significant Sharpe ratio of 0.56 (t-statistic of 8.22) from 1800 to 2020 and is positive in 89% of the 10-year rolling periods.

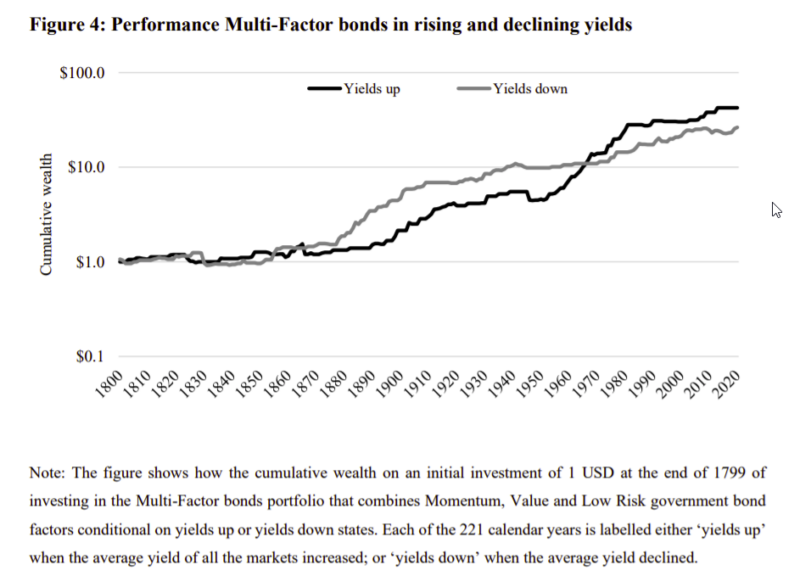

- A multi-factor bonds portfolio gives robust performance over various macroeconomic states like recessions and expansions, crisis and non-crisis periods, years with either rising or declining yields, years with above or below median inflation, and years with positive or negative equity returns.

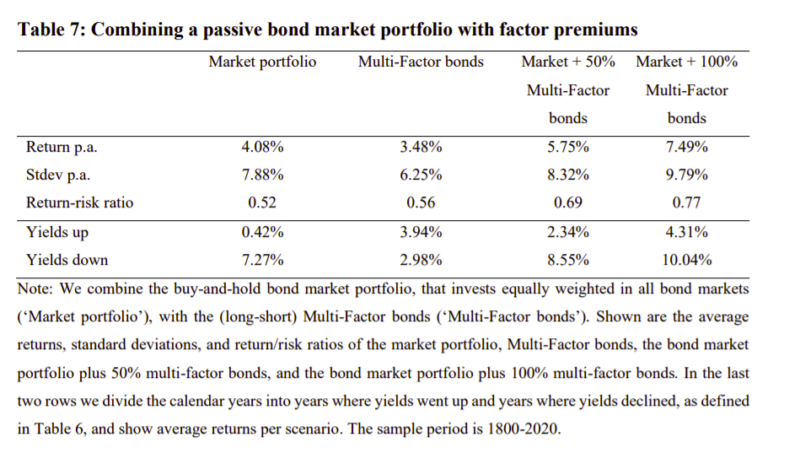

- There is a strong value add of a multi-factor bonds portfolio to an existing allocation: a multi-factor bonds portfolio has an average return of 3.48% a year at a correlation of –0.05 with the bond market and adding a multi-factor bonds strategy to a passive global government bond portfolio increases returns substantially with little impact on risk.

Why does it matter?

This paper is an important addition to the academic debate on factor investing. In particular, it adds important and robust evidence to the fact that factor strategies in government bonds offer attractive returns and diversify each other. They do so in both a long-short and long-only constrained setting.

The Most Important Chart from the Paper:

Abstract

We examine government bond factor premiums in a deep global sample from 1800 to 2020 spanning the major markets and maturities. Bond factors (Value, Momentum, Low-risk) offer attractive premiums that do not decay across samples, are persistent over time, and consistent across various market and macroeconomic scenarios. The factor premiums diversify to each other, as well asto bond or equity market risks. A combined multi-factor bond strategy provides the strongest risk-adjusted returns. These results strongly show a consistent added value of

government bond factor premiums over a passive bond portfolio.