Extrapolative Beliefs in the Cross Section: What Can We Learn from the Crowds?

- Zhi Da, Xing Huang, Lawrence J. Jin

- Journal of Financial Economics, 2020

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Historically, as Richard Thaler pointed out in his book Misbehaving, financial academics have looked at humans as “Econs.” An Econ, unlike a human, values everything down to a penny before they make a decision, knows all possible alternatives, weighs them accurately, and always optimizes. 1

In recent years we’ve moved away from thinking of humans as Econs. We are now left with the age-old question: How do humans form expectations about future asset returns? The literature provides convincing evidence of return extrapolation, the notion that investors’ expectations about an asset’s future return are a positive function of the asset’s recent past returns. However, there is less direct evidence on how investors form expectations about individual stock returns, whether these expectations are rational, and how they relate to subsequent returns.

Based on the sample used in this study, one thing is clear: don’t buy crowdsourced investment ideas!

What are the Academic Insights?

By analyzing a novel dataset from Forcerank ( a crowdsourcing platform for ranking stocks), the authors find 2:

- Individuals extrapolate from a stock’s recent past returns when forming expectations about its future return. In fact, the coefficients on distant past returns are in general lower than those on recent past returns: quantitatively, returns four weeks earlier are only about 9% as important as returns in the most recent week.

- The extrapolative pattern remains almost identical after controlling for past fundamental news, news sentiment, and risk measures

- Investors put more weight on negative past returns, and this weight decays more slowly into the past for negative returns.

- An individual stock’s return relative to its peer performance also seems to affect investor beliefs.

- Compared to nonprofessionals, financial professionals display a lower degree of extrapolation suggesting that professionals rely less on past stock returns when forming expectations about returns over the next week. Additionally, professionals’ expectations rely on past returns over a longer history.

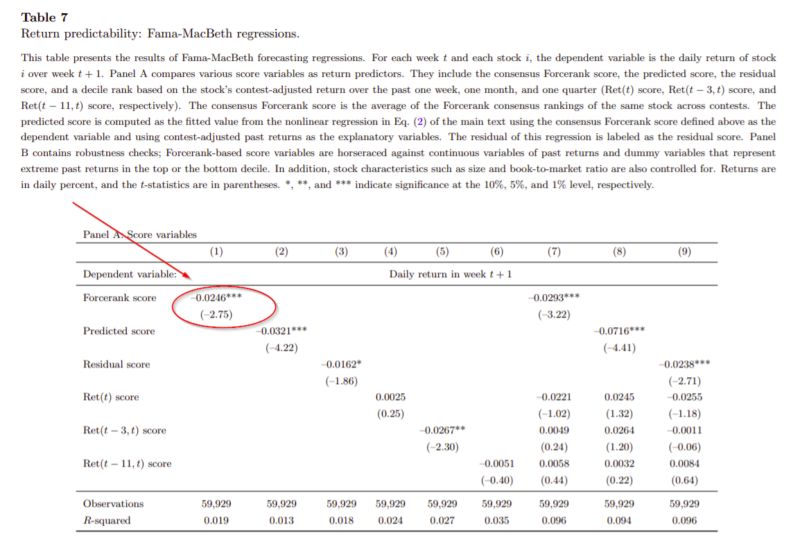

- Consensus Forcerank score significantly predicts future stock returns with a negative sign suggesting that beliefs of Forcerank users are systematically biased.

- Return predictability of the Forcerank score is stronger among stocks with lower institutional ownership and a higher degree of extrapolation.

Why does it matter?

Overall, the authors interpret the evidence as suggesting that the beliefs of these Forcerank users represent the thinking process of a broader group of behavioral investors in the market. Consistent with the beliefs of Forcerank users, extrapolators form expectations about the future returns of individual stocks by extrapolating from the recent past returns

of these stocks, and they trade stocks according to these extrapolative beliefs. Fundamental traders, on the other hand, serve as arbitrageurs who correct for mispricing. However, these traders are risk-averse and hence cannot completely undo the mispricing caused by extrapolators.

The Most Important Chart from the Paper:

Abstract

Using novel data from a crowdsourcing platform for ranking stocks, we investigate how investors form expectations about stock returns over the next week. We find that investors extrapolate from stocks’ recent past returns, with more weight on more recent returns, especially when recent returns are negative, salient, or from a dispersed cross-section. Such extrapolative beliefs are stronger among nonprofessionals and large stocks. Moreover, consensus rankings negatively predict returns over the next week, more so among stocks with low institutional ownership and a high degree of extrapolation. A trading strategy that sorts stocks on investor beliefs generates an economically significant profit.

Notes: