Traditional measures of geopolitical risk have been primarily qualitative. In this article, the authors describe and analyze not just new, but novel measures including textual analysis of news and expert reports, novel econometric methods and machine learning applications for measuring geopolitical risk and changes in geopolitical risk.

Comparing Geopolitical Risk Measures

- Ahmet K. Karagozoglu, Na Wang, and Tianpeng Zhou

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

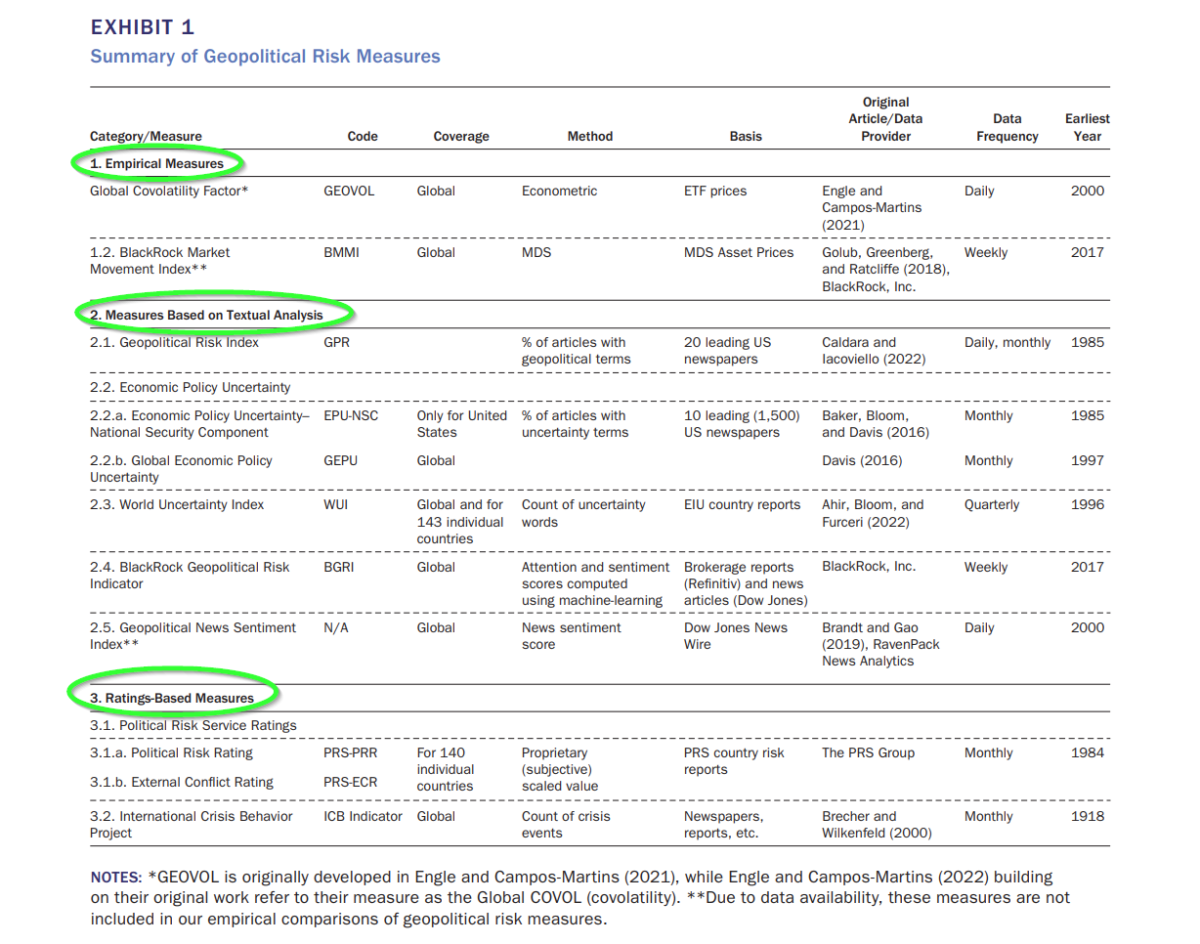

The set of novel geopolitical risk measures analyzed were grouped into three categories: Empirical measures (n=2), Textual analytical measures (n=6), and Ratings-based measures (n=3). Altogether, there were 11 measures, 2 of which lacked adequate data. All measures are described in Exhibit 1. Note the measures are observed on a daily, weekly, monthly or quarterly basis and that the original article and data source are also identified. A quick review of representative measures:

Empirical: For example, GEOVOL (observed daily) is a statistical estimate of the sensitivity of the actual price changes of financial assets due to volatility shocks to financial markets. Using the unsystematic portion of volatility of returns, the measure captures common volatility shocks affecting global markets. Consequently, investors and other market participants are able react very rapidly to changes in geopolitical risk by trading assets and hence incorporating new information into prices.

Textual: Textual analysis of newspaper articles, expert opinions, and other miscellaneous communication captures issues that people are worrying about or issues that might happen. Although the specifics used to construct the measure vary, they generally calculate the relative frequency of published articles and topics devoted to political risk.

Ratings-based: Ratings use the number of past geopolitical events or past information to make predictions of future geopolitical risks. Inputs could include the ICB Indicator or past PRS ratings.

- Are novel geopolitical risk measures positively correlated?

- Do the empirical measures based on asset prices such as GEOVOL, reflect geopolitical risk changes more promptly than textual analysis measures?

- Do the measures based on textual analysis reflect geopolitical risk changes more promptly than those based on ratings?

What are the Academic Insights?

- YES. For the most part the risk measures analyzed were positively correlated and statistically significant, especially between GEOVOL and the textual analysis–based measures. Among the daily geopolitical risk measures, the correlations ranged from 0.047 to 0.932, all significant. Among the measures calculated weekly, the correlations ranged from 0.031 to 0.178, 2 of 3 were significant. Among the measures calculated monthly, the correlations ranged from -0.303 to 0.679, all were significant with one exception.

- YES. The authors conducted lead-lag tests (vector autoregression models) to determine which, if any, risk measures dominate in terms of capturing changes in geopolitical risk. As expected, the empirical measures based on asset pricing reflected changes faster than textual and ratings-based measures. The strong correlation produced in the analysis argues for the validity of all measures as reflections of geopolitical risk. But what explains the relative superiority of empirical measures vs. textual vs. ratings-based approaches? Not surprisingly, the empirical and textual measures are superior instruments. They are constructed from prices of securities, published articles, newspapers, brokerage reports, all items that are “ex-ante” reflections of the market’s interpretation of geopolitical risks.

- YES. As expected, textual-based measures respond more rapidly to changes in geopolitical risks than ratings-based measures. The best example of a textual measure of geopolitical risk is the GPR Index, which is constructed by calculating the portion of articles that focus on threatening geopolitical issues and events in major English language newspapers. Ratings are typically constructed from expert reports of current and recent events which makes it an “ex-post” risk measure. It would be reasonable to expect the ratings measure to be a relatively weak predictive instrument.

Why does it matter?

I highly recommend this article. There are a number of contributions this article makes to any one of market participants (investors, portfolio managers, regulators, risk managers, traders). First the ability to identify, regulate and manage geopolitical risk. Second, a comprehensive introduction to the area of geopolitical risk, how it is measured and the level of validity for each type of geopolitical measure.

The most important chart from the paper

Abstract

Although geopolitical risk has traditionally been approached from a qualitative aspect, what makes it a novel risk is the application of innovative techniques to measure it. The authors compare methodologies and applications of geopolitical risk measures constructed using three broad approaches: empirical models of asset prices, textual analysis of news, and analyst/expert ratings. The authors examine the ability of these approaches to capture changes in geopolitical risks in a timely manner, and they document that measure based on asset prices reflect geopolitical risk changes more promptly than those based on textual analysis, whereas textual analysis–based measures incorporate new information on

geopolitical risk more promptly than ratings-based ones.