The Myth of Diversification Reconsidered

- William Kinlaw, Mark Kritzman, Sébastien Page, and David Turkington

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Diversification has been around since the early 1950s and is often considered a “free lunch” in finance. But is that actually the case? We’ve highlighted here and here that the reality is more complicated than the theory. Consider the two basic assumptions about correlations in the context of mean-variance optimization: (1) Pair-wise correlations are assumed to be symmetrical relative to rising vs declining returns—they are, in fact, asymmetrical; (2) Diversification is assumed to be desirable when assets are rising and when they are declining—a questionable assumption.

This article examines the extent to which these assumptions hold and the extent to which investors should want them to hold. The authors deliver a clever quote from Mark Twain (or maybe it was Robert Frost) that nails the issue in simple terms: “Diversification behaves like the banker who lends you his umbrella when the sun is shining but wants it back the minute it begins to rain”. Nicely expressed!

In addition to using Monte Carlo simulations, the authors analyzed data on six benchmark indexes to represent six asset classes(1). The data was obtained from Datastream and covered the period January 1976 to December 2019. Data on emerging markets begin in January 1988. The following questions were addressed.

- Does diversification always benefit investors?

- How is correlation asymmetry measured?

- Do asset classes exhibit correlation asymmetry?

- What should investors do about it?

What are the Academic Insights?

- NO. The authors argue that while diversification is beneficial to investors on the downside, investors should prefer that it disappear when assets move in concert in an upward direction. In other words, Investors should seek out sources of diversification (-ρ) when assets are moving to the downside and “unification” (+ρ) when assets are moving to the upside.

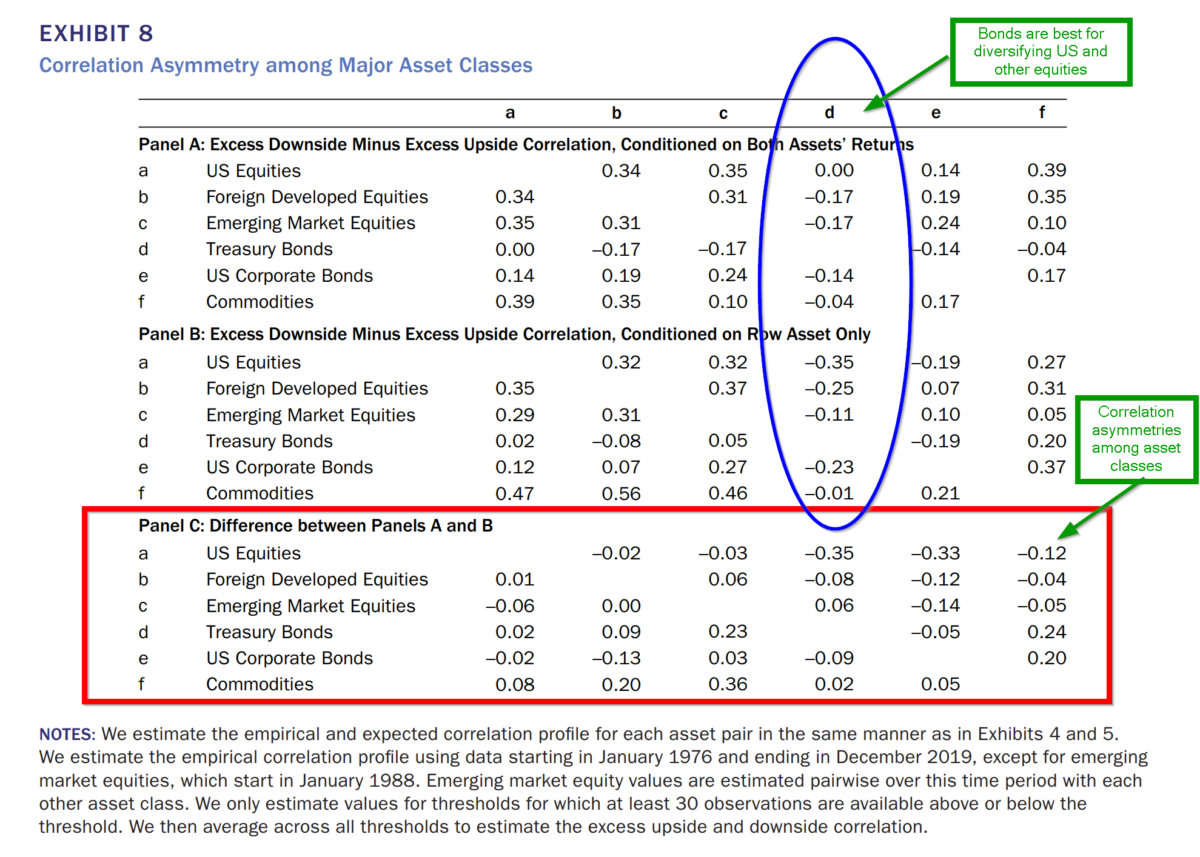

- Correlation asymmetry is calculated for each asset class pair as the average difference between the empirical downside (and upside) correlation calculated at a threshold value for down and a threshold value for up markets(2). The correlations are calculated against two separate thresholds: one for an upside or downside threshold against one asset only or against a threshold for both assets.

- YES. The results are presented in Exhibit 8 below. Note that emerging equity markets, international developed equity markets, and commodities exhibit the least attractive correlation asymmetries for US equities. However, Treasury and corporate bonds exhibited the most attractive qualities in terms of asymmetry. Further, Treasuries are universally attractive to all other asset classes when correlations are conditioned by thresholds. However, it appears that diversification potential appears larger when the correlation is calculated against a threshold for a single asset class. CAVEAT: interest rates are currently very low and price movement may be limited as a result. Commodities exhibited a negligible potential under either type of threshold conditioning.

- TWO OPTIONS ARE DISCUSSED. First, if regime shifts in the markets are expected then investors could increase allocations to “safe-haven” assets if the expectation is negative. This approach essentially requires investors to take a predictive stance with respect to which correlations are most likely to emerge in the future. Or, assign a larger weight to downside correlations when policy weights are being determined. This requires the investor to take a preparation approach by incorporating assets that would provide sufficient resilience during downturns.

Why does it matter?

The major contribution of this article lies in the application of the findings. We would recommend the interested reader to explore more fully the discussion of the third alternative for investors, a very technical method, that allows the use of full-scale portfolio optimization in the context of correlation asymmetry. The authors demonstrate that It is well within the reach of investors to use full-scale optimization to construct portfolios that account expressly for various asymmetric correlation situations. You can also reach out and set up a discussion on the topic of building robust portfolios that don’t suffer from poor correlation assumptions.

The most important chart from the paper

Abstract

That investors should diversify their portfolios is a core principle of modern finance. Yet there are some periods in which diversification is undesirable. When the portfolio’s main growth engine performs well, investors prefer the opposite of diversification. An ideal complement to the growth engine would provide diversification when it performs poorly and unification when it performs well. Numerous studies have presented evidence of asymmetric correlations between assets. Unfortunately, this asymmetry is often of the undesirable variety: It is characterized by downside unification and upside diversification. In other words, diversification often disappears when it is most needed. In this article, the authors highlight a fundamental flaw in the way some prior studies have measured correlation asymmetry. Because they estimate downside correlations from subsamples in which both assets perform poorly, they ignore instances of successful diversification (i.e., periods in which one asset’s gains offset the other’s losses). The authors propose instead that investors measure what matters: the degree to which a given asset diversifies the main growth engine when it underperforms. This approach yields starkly different conclusions, particularly for asset pairs with low full-sample correlation. The authors review correlation mathematics, highlight the flaw in prior studies, motivate the correct approach, and present an empirical analysis of correlation asymmetry across major asset classes.